Thesis

DoorDash is a delivery network being turned, step by step, into the operating system for local commerce. It is becoming the layer that sits between consumers, merchants, and last-mile fulfillment for anything a neighborhood can buy.

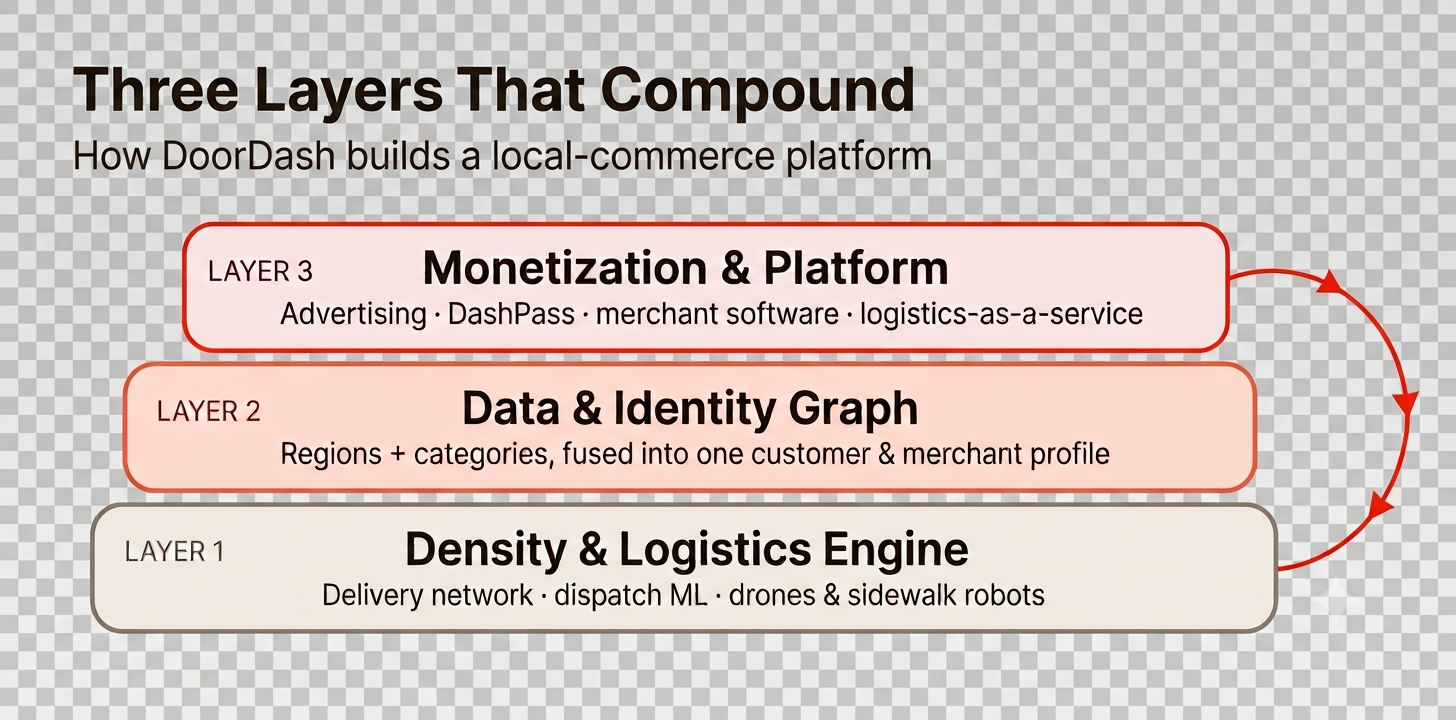

The build follows a clear order, and the order matters more than any single piece. First, a delivery network that gets better the denser it gets. Then the network widens along two axes: across regions, and across categories, all folded into one platform. Only after that does the money-making stack go vertical, with advertising, DashPass, merchant analytics, logistics-as-a-service, and storefront software layered on top of infrastructure that already exists. The endpoint is a single platform a business can run its entire local operation on, and a single app a consumer can buy anything local from.

What makes it work is that every step feeds the same two flywheels, one for logistics and one for data. Each move makes the next one cheaper to pull off and more valuable once it is live. Delivery is the foundation and it pays for everything above it, but it is not where the value ends up.

The Build Order

1. A delivery network that compounds on density

The base layer is a two-sided marketplace where density is the whole game. More consumers in a market pull in more merchants, and more merchants widen selection, which pulls in more consumers. Each side reinforces itself and the other. Density also pays off in the logistics itself: more orders per square mile means more orders per Dasher-hour, which lowers the cost of each delivery, which lowers prices and wait times, which drives still more orders. The customer-merchant loop and the logistics loop run on the same fuel.

The core of this is a fact about geometry, not just business. The length of an efficient delivery route over N stops in an area A grows only like the square root of A times N, so in a denser area each extra customer adds barely any additional driving and the cost per drop keeps falling as orders per square mile rise. That declining marginal cost is the mathematical root of the whole flywheel, and it is why density, rather than raw scale, is what actually matters.

DoorDash has processed well over 900 million orders since it started, and it holds roughly 67% of U.S. restaurant delivery. That means it sees more real dispatch outcomes than all of its domestic rivals combined, and its routing models get better with every one of those orders. You cannot buy that data, you have to accumulate it, which is exactly why a new entrant cannot copy it. The 2025 Metis acquisition pushes dispatch from reactive routing toward a system that learns to negotiate local capacity on its own, lowering the baseline cost per delivery over the next several years.

The cost curve keeps bending from here. DoorDash is layering autonomous delivery on top of the human fleet, through drone partnerships (including Wing) and sidewalk robots for short-range orders. Each of these takes cost and time out of the cheapest, densest routes first, which is the same lever that started the flywheel. Autonomy is not a separate story, it is the delivery layer getting cheaper, and a cheaper delivery layer makes everything above it easier to justify.

2. Widen the network horizontally

Once the density engine works in one place, the cheapest growth is to run it again somewhere else, and to run it on more kinds of goods. These are two axes of the same move.

Across regions, Wolt (2022) and Deliveroo (completed October 2, 2025) extended the network to more than 40 countries and gave DoorDash leading positions across Western Europe. The point is not just a bigger map. It is that these regional networks are folded into one platform, with a single logistics brain, one merchant toolset, and, most importantly, one consumer data graph. That consolidation is what later makes the advertising business credible. Coca-Cola will not buy ad inventory from a platform with 10% share in Germany, but at dominant share across a region the conversation is different.

Across categories, a dense network makes adding a new vertical almost free at the margin, because the Dashers, the routing, and the ordering habit already exist. DoorDash went from restaurants into grocery, alcohol, convenience, pets, beauty, and retail including electronics. Every new category is attractive from all three sides at once. Consumers get closer to buying anything local in one app, which raises how often they open it. Merchants join because the demand is already sitting there. And DoorDash widens the behavioral dataset that powers everything downstream.

The keystone of this phase is SevenRooms (roughly $1.2B, 2025), a reservation, CRM, and guest-data platform for restaurants and hotels. It is less a delivery category than a bridge, connecting what a customer orders online to how they behave in person and inside a venue. That link is what no rival advertising platform has, and it sets up the vertical stack.

3. Monetize vertically on shared infrastructure

Only after density, geography, and categories are in place does DoorDash go vertical, making money off the same infrastructure in several ways at once:

- Advertising: promoted listings, sponsored search, and CPG campaigns priced against first-party purchase data. The extra gross margin on an ad approaches 100% because it needs no extra Dasher and no fulfillment cost.

- DashPass and Wolt+: subscriptions (in the U.S., $9.99 a month or $96 a year) that zero out delivery fees, lifting frequency and locking in the habit.

- Merchant analytics and CRM: turning the guest-data graph into a product merchants pay for.

- Logistics-as-a-service (Drive): a white-label API that lets any merchant rent the Dasher network without showing up on the marketplace. Spare delivery capacity sold the way AWS sells spare compute.

- Storefront software: tools that let merchants run their own ordering channels, which moves DoorDash from vendor to infrastructure, the same path Shopify took.

DoorDash today

~0.8%

est. ad attach rate

Instacart benchmark

3.5%

mature commerce media

Revenue at Instacart rate

$2-3B

high-margin, unpriced

Ad attach rate (advertising revenue as % of GMV). DoorDash at ~0.8% today vs. 3.5% for mature commerce media peers. The gap is the unpriced optionality.

Why the Order Matters: the Data and Logistics Flywheel

The build order is not arbitrary. The monetization layers are impossible without density underneath them, and this is the strongest part of the thesis. A competitor can copy any one layer, an ad product, a subscription, a merchant tool, but it cannot copy the order or the data that piles up along the way. That is where the compounding lives.

Density drives everything downstream. The dense two-sided network reliably supplies both customers and merchants, and both sides feed themselves. That same density is what makes adding categories cheap: new goods reach the customer quickly and affordably, merchants sign up because the demand already exists, and consumers consolidate their spending because they can get everything in one place.

Breadth of categories sharpens the data, not just the selection. Every order is both a sale and a data point, but variety matters more than raw volume. A customer who orders dinner, groceries, wine, pet food, and books a hotel reveals a far richer profile than one who only orders dinner. More categories mean more accurate customer profiles, which mean better ad targeting. After Apple’s privacy changes gutted cookie-based targeting, real purchase behavior became the highest-signal input in advertising, and DoorDash’s breadth is exactly what makes its profiles high-signal.

Accurate profiles let DoorDash sell advertising beyond its own app. Because the profiles are precise, DoorDash can target consumers off-platform, across search, social, and display, and still close the loop on attribution (Symbiosys, 2025), with privacy-safe matching to brand datasets through LiveRamp clean rooms. The ad business stops being a subsidy for delivery and becomes a customer-acquisition engine that brands buy for its own sake.

The same graph lets merchants find each other’s customers. Because one identity spans restaurants, retail, and hotels, DoorDash can send a hotel guest to a nearby restaurant, or a grocery buyer to a new CPG product. Merchants reach genuinely new customers through the graph, which no single-category platform can offer.

Breadth and depth both make DashPass more compelling. Breadth, because once you can buy everything in one place, a subscription that zeroes delivery fees across all of it is worth far more. Depth, because as DoorDash integrates into restaurants and hotels through SevenRooms, it can fold in-person perks into DashPass, like priority reservations, loyalty, or member pricing. More reasons to subscribe means more subscribers, higher frequency, and more data, which loops back to the top.

The loop closes inside the merchant. The customer profile DoorDash builds online can flow back into the tools it sells the merchant: the POS, the reservation book, the CRM. A restaurant that greets a guest already knowing their order history, their allergies, and how much they usually spend serves them better, sells more, and gets harder to leave. Better guest experience and higher merchant sales feed right back into the data and density that started the whole thing.

Put simply, three loops run on one engine. More orders make the routing better, which lowers cost, which lowers prices, which brings more orders. DashPass turns casual users into subscribers, who order more often, which justifies wider selection, which wins more subscribers. And dense, varied data buys premium targeting on and off the platform, which throws off high-margin revenue, which funds the subsidies that bring in the next subscriber and the next data point. When DoorDash sells one more ad, the extra cost is close to zero, so as advertising grows as a share of revenue, the whole margin profile lifts even if delivery margins stay flat.

The Endpoint: One Platform for the Business, One App for the Consumer

Stack these layers together and the ultimate state of the thesis comes into view. Once physical delivery, payments, analytics, marketing, reservations, and software all run through DoorDash, a local business no longer strings together five vendors, it runs its operation on one platform. Demand, fulfillment, customer data, and marketing come from the same place, and each one works better because the others are there. That is a far stickier relationship than any single product could ever be, and it is the natural end of the build.

The consumer side is the mirror image. The same integration that gives the merchant one platform gives the consumer one app for everything local, from dinner to groceries to a hotel booking, with a single subscription and a single profile behind it. Both sides converge on the same idea from opposite directions, and DoorDash sits in the middle of it.

The Acquisition Architecture

Each 2025 acquisition fills a specific gap in the build order:

- Deliveroo (roughly $3.9B): completed the European map, giving DoorDash dominant positions across about 45 countries and the global scale that a serious advertising business requires.

- Metis: upgraded dispatch from reactive routing toward a system that manages local capacity by learning, which lowers the baseline cost per delivery.

- Symbiosys ($175M): closed-loop measurement across the open internet, so first-party purchase data can target consumers on any digital channel.

- SevenRooms (roughly $1.2B): the keystone, connecting delivery data to in-store and in-venue behavior and closing the consumer identity graph. No advertising platform can currently trace a digital ad all the way to an in-person restaurant or hotel visit with purchase-level accuracy. DoorDash will be able to.

FY2025 Financials in Brief

FY2025 is the year operating leverage showed up. Revenue reached $13.7 billion, up 28% year over year, on Marketplace GOV of $102 billion, up 27%. GAAP gross profit was $6.686 billion (6.6% of GOV, up from 6.2%). Adjusted EBITDA was $2.779 billion, up 47%, and GAAP net income was $935 million, against $123 million in FY2024 and a $558 million loss in FY2023. In three years the business went from real losses to nearly a billion in GAAP profit, which is what crossing critical density in the core markets looks like.

The number that matters most is Net Revenue Margin (revenue divided by GOV), which was 13.4%, roughly 50 basis points above two years earlier, with more expansion guided as advertising grows as a share of revenue. Each 100 basis points of that margin on $100 billion of GOV is a billion dollars of revenue at almost no extra cost. Operating expenses are growing far slower than revenue, so the path toward 20%-plus EBITDA margins, which Meituan has already walked in China, is a few years out but visible from here. The model is also unusually asset-light: the Dasher fleet is off the balance sheet, capital spending looks like a software company’s, and free cash flow inflected positive in FY2024 and grew in FY2025.

Where the Market May Be Wrong

DoorDash is still priced mostly as a delivery platform, even though it is increasingly a three-part company, delivery plus subscription plus advertising, all riding one data and logistics flywheel. The advertising business, estimated at $750-900M and growing more than 60% in 2025, is structurally higher-margin and more scalable than logistics. If DoorDash Ads reaches $2.5B by 2027, it stops being a subsidy for delivery and becomes a profit engine in its own right.

The Amazon parallel is structural, not casual:

| DoorDash Product | Amazon Equivalent |

|---|---|

| Marketplace delivery | Amazon Marketplace |

| DoorDash Drive | Fulfillment by Amazon |

| DashPass | Amazon Prime |

| DoorDash Ads + Symbiosys | Amazon Advertising DSP |

| Storefront + SevenRooms | AWS |

The difference is what each one knows about you. Amazon knows what you bought online. DoorDash, with SevenRooms and Symbiosys, will know what you bought online, what you ordered for delivery, which restaurants and hotels you walked into, and how you reacted to ads across channels. For food and local commerce, that is a more complete picture of a customer than any platform has today.

Delivery is how it got here. It is not where it is going.

Prepared by Consti Ertel | March 1, 2026 | For informational purposes only. Not investment advice.